M/S Mansi Finance (Chennai) Ltd. v. M. Lalitha & Ors. | 2026 INSC 547 | Criminal Appeal No. 2849 of 2026

Bench: Justice Prashant Kumar Mishra & Justice N.V. Anjaria | Decided: 26 May 2026

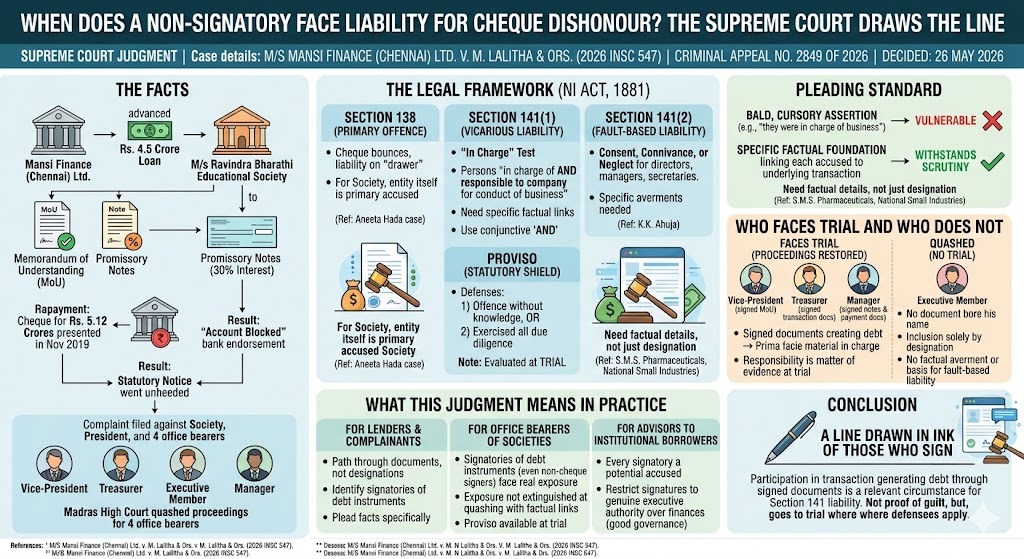

Cheque dishonour litigation in India has a well-worn pattern: when a cheque bounces, creditors name every traceable office bearer of the drawer entity; President, Vice-President, Treasurer, Manager, Executive Member, on the assumption that at least some names will stick. Courts have repeatedly refused to accept designation as a substitute for criminal culpability. What the Supreme Court has now done in M/S Mansi Finance (Chennai) Ltd. v. M. Lalitha & Ors.,decided on 26 May 2026, is to clarify with precision where the line falls, not just as a matter of pleading, but as a matter of proof.

The Facts

In July 2018, Mansi Finance (Chennai) Ltd. advanced Rs. 4.5 crore to M/s Ravindra Bharathi Educational Society, registered under the Societies Registration Act, 1860. The loan was evidenced through a Memorandum of Understanding and promissory notes carrying interest at 30 per cent per annum. A cheque for Rs. 5,12,61,500 was drawn towards repayment and, when presented in November 2019, was returned with the bank endorsement “Account Blocked.” A statutory notice under Section 138 of the Negotiable Instruments Act, 1881 went unheeded, and Mansi Finance filed a complaint before the Metropolitan Magistrate, Chennai, under Sections 138 and 141 of the NI Act.

Along with the Society and its President, the complaint named four office bearers as accused: the Vice-President, Treasurer, an Executive Member, and the Manager. All four moved the Madras High Court under Section 482 of the Code of Criminal Procedure, 1973, and succeeded. The High Court quashed proceedings on the ground that the complaint contained only omnibus allegations without the specific averments required for vicarious liability. Mansi Finance appealed to the Supreme Court.

The Legal Framework: Sections 138 and 141 of the NI Act

Section 138: The Primary Offence.Section 138 of the NI Act creates the primary offence of dishonour of a cheque and attaches criminal liability directly to the drawerof the instrument. Where the drawer is a non-natural entity, a company, firm, or, as here, a registered society. The entity itself is the primary accused. A registered society falls within the Explanation to Section 141, which defines “company” to include “any body corporate and includes a firm or other association of individuals.” This is the jurisdictional hook for the prosecution of office bearers: the Society was arraigned as accused No. 1, satisfying the foundational precondition reinforced in Aneeta Hada v. Godfather Travels & Tours (P) Ltd.1,that the entity must be made an accused before its office bearers can face vicarious liability at all.

Section 141(1): The “In Charge” Test.Section 141(1) extends criminal liability to every person who, at the time the offence was committed, was “in charge of, and was responsible to the company for the conduct of the business.” The Supreme Court in Ashok Shewakramani v. State of Andhra Pradesh2, held that these two limbs must be read conjunctively, the use of the conjunction “and” is deliberate. Merely managing some aspect of the entity’s operations is not enough; the accused must satisfy both conditions simultaneously. Designation as an office bearer, without more, does not discharge this burden on the complainant.

Section 141(2): Consent, Connivance, or Neglect.Section 141(2) provides a separate and distinct head of liability for directors, managers, secretaries, and other officers of the entity. Liability here does not depend on holding executive charge; it attaches where the offence is committed with the officer’s consent or connivance,or is attributable to any neglect on his part. Per K.K. Ahuja v. V.K. Vora3, officers who are neither a Managing Director nor a Joint Managing Director, and who did not sign the dishonoured cheque, can be roped in only through this fault-based route and the complaint must contain specific averments to that effect.

The Proviso: Statutory Escape Hatch.The proviso to Section 141(1) carves out a defence for accused persons who can prove either that the offence was committed without their knowledge, or that they exercised all due diligence to prevent it. This is the principal shield available to signatories whose prosecution is restored to trial, The question of whether they can successfully invoke the proviso is precisely the kind of inquiry that must unfold before the trial court, not be pre-empted at the quashing stage.

The Pleading Standard.The settled position from S.M.S. Pharmaceuticals Ltd. v. Neeta Bhalla4Bhalla4 is that a complaint must specifically aver that the accused was in charge of and responsible for the conduct of the business, mere designation as a director or office bearer is insufficient. National Small Industries Corporation Ltd. v. Harmeet Singh Paintal5reinforced that Section 141, being a penal provision creating vicarious liability, must be strictly construed: a bald, cursory assertion will not do. HDFC Bank Ltd. v. State of Maharashtra6introduced a necessary corrective: substance over form. A complaint need not reproduce the exact statutory phraseology; what matters is whether, read as a whole, it discloses a sufficient factual foundation linking each accused to the underlying transaction. The Court’s inquiry at the quashing stage is limited to whether there is a prima facie basis to proceed, not whether guilt is made out.

Who Faces Trial and Who Does Not

The Court examined precisely what each of the four respondent office bearers had signed. The Vice-President had signed the MoU. The Treasurer had signed the transaction documents. The Manager had signed the promissory notes and allied payment documents. All three had placed their names on instruments that created, recorded, and acknowledged the very debt for which the cheque was eventually drawn and dishonoured.

The Executive Member stood in an entirely different position: not a single document in the record bore his name, not the MoU, not the promissory notes, not the cheque. His inclusion in the complaint rested solely on his designation as a member of the Society’s executive.

The Supreme Court was unambiguous. Participation in the transaction, demonstrated through signed documents, constituted prima facie material establishing that the Vice-President, Treasurer, and Manager were in charge of the affairs of the Society within the meaning of Section 141. Whether they were in fact responsible is, as the Court expressly acknowledged, “ultimately a matter of evidence to be established at trial”, not a question to be foreclosed at the threshold. Proceedings against all three were restored.

For the Executive Member, the Court upheld the quashing. No factual averment linked him to the transaction. Designation alone cannot attract criminal liability under Section 141, and the complaint disclosed no basis to bring him within Section 141(2) either.

What This Judgment Means in Practice

For lenders and complainants:The path to a durable prosecution under Section 141 runs through documents, not designations. Identifying which office bearers signed the loan agreement, the MoU, or the promissory notes and pleading those facts specifically will withstand scrutiny at the quashing stage. Complaints that rest on a bare assertion that the accused “were in charge of the business” remain vulnerable to Section 482.

For office bearers of societies and institutions:A signatory to debt-creating instruments, even one who did not sign the dishonoured cheque itself faces real exposure under Section 141. That exposure cannot be extinguished at the High Court stage once the complaint discloses sufficient factual material. The proviso to Section 141(1) remains available at trial: an accused who can demonstrate that the offence occurred without his knowledge, or that he exercised all due diligence, may still escape conviction.

For advisors to institutional borrowers:Every signatory to a loan agreement, MoU, or promissory note is a potential accused in any future cheque dishonour complaint. Restricting such signatures to individuals with genuine executive authority over the institution’s finances is not merely good governance, it is sound legal risk management.

Conclusion

M/S Mansi Finance (Chennai) Ltd. v. M. Lalitha & Ors.clarifies that participation in the transaction that generated the debt evidenced through signatures on the MoU, promissory notes, or financial documents constitutes a relevant and proximate circumstance for establishing liability under Section 141. Signature on such documents is prima facie evidence that an accused was in charge of and responsible for the affairs of the entity; it is not, by itself, proof of guilt. That question remains for trial, where the proviso defences will come into play.

A Vice-President who signed the MoU, a Treasurer who signed the financial documents, a Manager whose name appears on the promissory notes: all three face trial. An Executive Member whose name appears nowhere in the paperwork does not. The Supreme Court has given the clearest articulation yet of where this line falls, and it is a line drawn in ink of those who sign.

References

1. Aneeta Hada v. Godfather Travels & Tours (P) Ltd., [(2012) 5 SCC 661]

2. Ashok Shewakramani v. State of Andhra Pradesh, [(2023) 8 SCC 473.]

3. K.K. Ahuja v. V.K. Vora, [(2009) 10 SCC 48.]

4. S.M.S. Pharmaceuticals Ltd. v. Neeta Bhalla, (2005) 8 SCC 89 (Three-Judge Bench).

5. National Small Industries Corporation Ltd. v. Harmeet Singh Paintal, (2010) 3 SCC 330.

6. HDFC Bank Ltd. v. State of Maharashtra, (2025) 9 SCC 653, 2025 INSC 759.